|

|

||||||

|

|

|

Wealth Insights

Lessons from the markets in 2021

A review of 2021 and the outlook for 2022 OCBC Bank

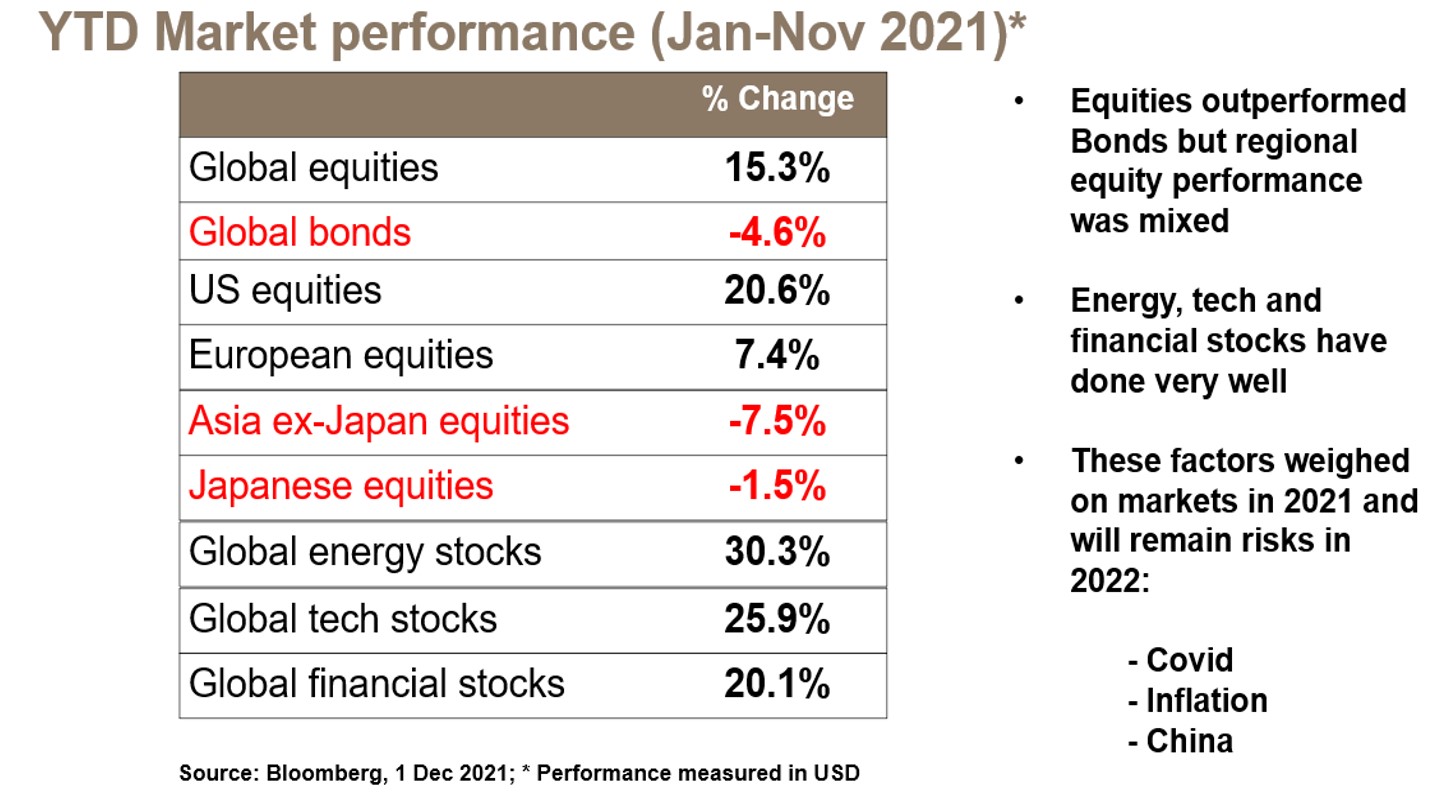

By all counts, 2021 should have been a down year for riskier assets like equities given the significant macro headwinds faced by markets since the start of the year and after a phenomenal 68% rally in global equities in 2020 from the post-Covid lows in late-March last year. However, this is not what happened. Instead, global stock markets continued to post positive returns in 2021, rising 15% in the first eleven months of the year. The US stock market was the star performer while Asian markets as measured by the MSCI Asia ex-Japan index fell due to the sharp sell-off in Chinese equities. Sector-wise the energy, tech and financial sectors stood out from the pack. A key lesson from 2021 is that it does not pay to be too cautious. Waiting for blue skies before investing is not an ideal strategy. Uncertainty will remain a fixture for many more years, so waiting for it to clear up completely before investing may mean missing attractive opportunities. A better strategy would have been to buy gradually over time (especially on significant pullbacks) instead of trying to time the markets. The other lesson from 2021 was that growth stocks like tech stocks; and value or cyclical stocks like financial and energy stocks, both managed to do well, and investors who had their money in either or both, would have done quite well. The MSCI World Growth Index was up 18% in the first eleven months of 2021 while the MSCI World Value Index was up 12%, underperforming the former but still posting a decent double-digit gain. There was a great deal of debate at the onset of 2021 as to whether tech stocks, which has done exceptionally well in 2020, would pass the baton to value/cyclicals stocks as economies re-opened after vaccines started getting administered late last year. Despite this, tech stocks have continued to do well while value stocks did decently too. There is clearly a place for both growth and value in investor’s portfolio and they are not mutually exclusive. Why did stock markets defy gravity in 2021? Markets faced several headwinds in 2021. This included concerns about rising inflation and fears of tighter monetary policy, rising bond yields, renewed concerns about the pandemic as a new Covid variant (Omicron) surfaced in late November, and concerns about China where stock markets plunged, property developers ran into problems and the economy experienced a sharp slowdown due to tighter credit, a resurgence of Covid and power outages. So, markets had a lot to worry about in 2021, and yet, the MSCI World Index which measures global equities still managed to stage a credible performance. Liquidity was a major factor that contributed to this. There was an abundance of liquidity on the side-lines as investors were looking for opportunities to buy. So, pullbacks were shallow and when they did happen, idle money went to work, seeking bargains. Also interest rates have been ultra-low, especially real interest rates which are negative and close to historic lows. So, investors see little reason to keep their money in idle cash. However, at the same time, there is a healthy level of scepticism among investors which also explains the abundance of dry power. This is not necessarily a negative factor as it means that liquidity will remain supportive of the markets. We have not reached a stage of euphoria and irrational exuberance in markets, like the dotcom bubble in early 2000, which would be a red flag. Other factors that contributed to the stock market rally in 2021 was the continued dovishness by the US Federal Reserve (Fed) despite rising inflation, and the willingness of governments to continue providing fiscal policy support. All these, coupled with rising vaccination rates and Covid fatigue have improved reopening prospects and given rise to hope that economic growth will remain resilient even though a slowdown is inevitable from peak growth rates in the 2021. However, there were also asset classes that did poorly in 2021. Chinese stocks for one, bucked the trend and experienced a sharp sell-off. Bonds and gold were affected by rising yields while gold was also affected by the stronger US dollar which got a boost from rising yields. However not all bond markets did poorly. High yield bonds managed to outperform investment grade bonds and eked out small gains. What lies ahead in 2022? After the strong stock market rally in the past 21 months, investors are understandably nervous. Inflation is also adding to the jitters, and it will remain a key risk in 2022 that is sure to cause continued market volatility. Uncertainty about the latest Covid variant, Omicron, is also clouding the outlook for 2022. It will be few weeks before scientists get a better handle of the virus to assess how infectious and lethal it is. Valuations have become less attractive, but they are not yet excessive as real interest rates are still very low by historical standards and liquidity remain abundant. So, expect intermittent market pullbacks after a strong rally over the past two years or so. This is normal and not the start of a bear market. In fact, pullbacks can offer buying opportunities for those with a good risk appetite, although investors need to tread carefully, stay diversified, buy selectively, and buy gradually if they are keen to invest on pullbacks for the medium to long term. The easy money has been made but there is still money to be made. The returns going forward will moderate as monetary and fiscal policy becomes less accommodative compared to 2020/2021 and economic and earnings growth rates ease from their peaks in 2021. Other risk factor to bear in mind for 2022 besides Covid, inflation and rising interest rates include the Chinese economy and property market and the US mid-term elections in November 2022. On the other hand, if inflation does ease in 2022, as some major central banks have projected, this could lift sentiment for stock markets. Also, by this time next year, vaccination rates are likely to significantly higher and this may ease fears about Covid which should be good news for equities. In a nutshell, it may be too early to throw in the towel after nearly two good years for equity markets. However, this does not mean that you should throw caution to the wind either. Staying diversified and being selective are especially important at this juncture. Within our asset allocation strategy, we maintain a moderately risk-on stance, keeping our overall overweight position in equities with a preference for US equities. However, for prudence, investors should have a balance of assets in their portfolios including some exposure to bonds which tend to be generally less volatile than equities. Within the bond space, we remain overweight on emerging market high yield bonds and neutral on developed market high yield bonds. All in, 2022 could continue to be another decent year for markets as it was for 2021, provided inflation and Covid infections do not surge much more and cause significant problems.   Global Outlook

A Brave New World

Positioning for Continued Recovery OCBC Bank, Bank of Singapore

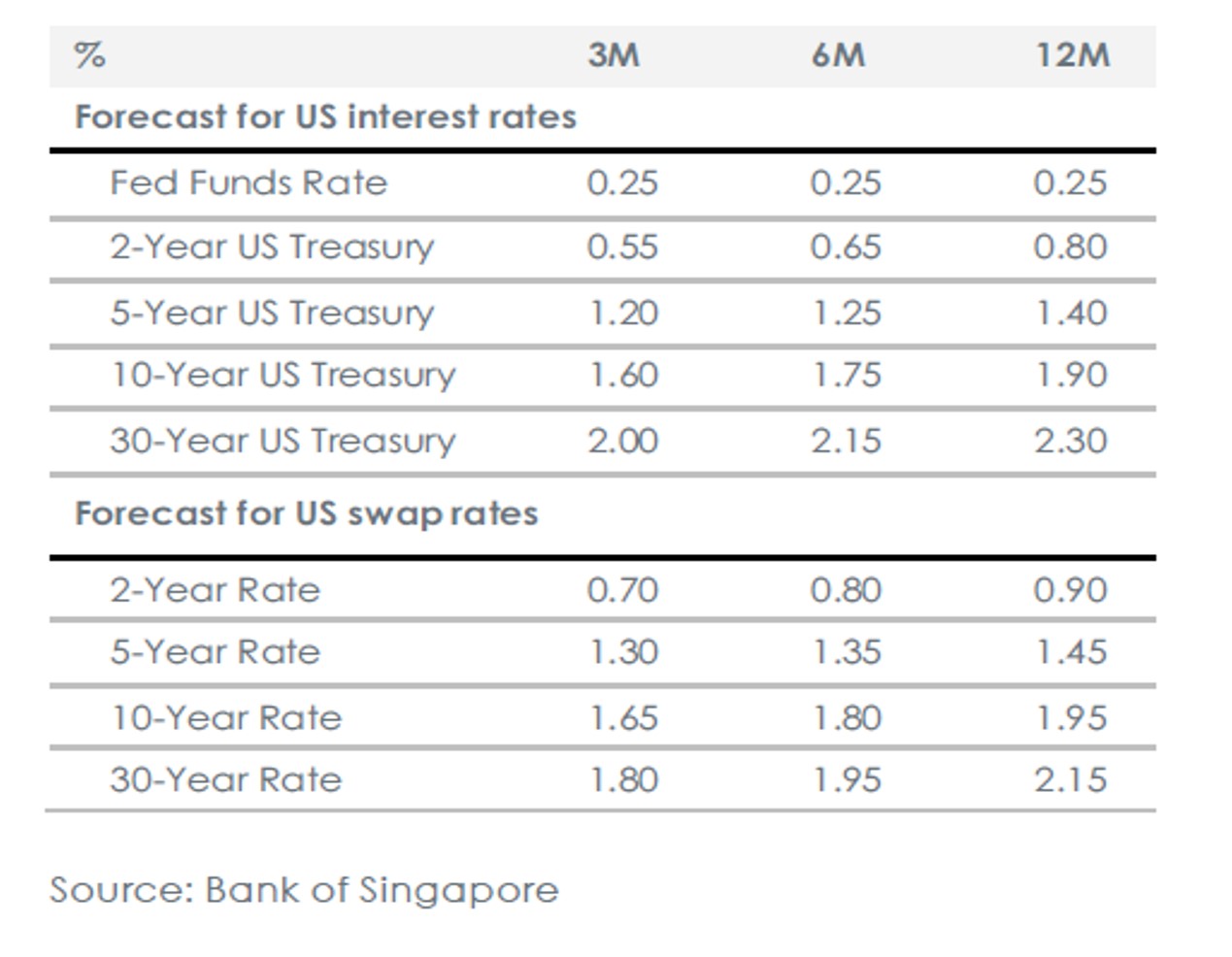

The global economy is again likely to expand strongly in 2022, following this year’s record rebound, as countries keep reopening from the pandemic. We expect the US, the Eurozone and the UK will grow sharply by 4.8%, 4.7% and 5.5% respectively in the new year. Japan’s growth is also likely to pick up to a robust 3.0% in 2022. And India is set to be the world’s fastest growing major economy with its GDP likely to expand by 9.0% both this year and next. In contrast, we anticipate China’s growth will slow significantly from a high 7.9% in 2021, following its earlier V-shaped recovery, to 5.5% in 2022. Beijing is likely to keep its zero-cases approach to the virus, implement strict lockdowns whenever fresh outbreaks occur and refuse to open up to the rest of the world while the pandemic continues. In the worst-case, China may remain isolated throughout next year. But we think global growth overall will be close to 5% in 2022. Thus, the world economy would, for the second year in a row, expand at a much faster pace than its average 3% annual rate recorded since the 1970s. But the new Omicron variant is concerning… The macroeconomic outlook, however, continues to face fresh risks. First, the new Omicron variant, initially identified in South Africa, may be a highly infectious strain of the virus, even more so than Delta, and could prove to be more resistant to currently available vaccines. The new variant appears to have an unusually high number of mutations, potentially reducing the effectiveness of existing vaccines. It may also be very contagious as cases have emerged outside southern Africa, in Europe and Asia. Moreover, the new strain could prove more lethal than earlier variants. With Europe already affected by a winter wave of infections from the Delta variant, Omicron has the potential to result in further lockdowns across the globe. The US, the European Union, the UK, Australia, Canada, Saudi Arabia and South Korea have quickly imposed travel restrictions on visitors from southern Africa. Israel and Japan have become the first countries to close their borders and the UK has made wearing masks compulsory again in shops and on public transport. It is likely to take researchers until the middle of December to assess how infectious Omicron is compared to other variants. By January, the impact on hospitalizations and fatalities will become clearer while pharmaceutical companies are likely to spend December seeing how effective existing vaccines are. If required, vaccine makers would likely need several months from Omicron’s discovery at the end of November to adapt their vaccines, gain regulatory approval and start shipping batches to counter the new variant. Thus, economic activity across the globe may be dented as 2022 starts. But the risks to growth from Omicron are likely to be tempered by the knowledge governments, central banks, companies, employees, and households have gained during the pandemic since the start of 2020. Officials are unlikely to impose stringent lockdowns except for China. Monetary policymakers are set to remain dovish if activity appears at risk, and the experience of this summer’s Delta waves shows economies bounce back quickly when infections recede as the chart above of purchasing manager indices (PMIs) shows. …and inflation is proving to be sticky The second risk to the outlook is inflation. Consumer prices are rising by more than 6.0% YoY in the US and over 4.0% YoY in the UK and Eurozone. Soaring demand from economies reopening and supply disruptions are pushing inflation up to levels last seen thirty years ago in western economies. In contrast, inflation across Asia is more muted, running at 1.5% YoY in China and just 0.1% YoY in Japan as the region, being the home to much of the world’s manufacturing, is less vulnerable to supply glitches. For now, the major central banks including the Federal Reserve, the European Central Bank (ECB), the Bank of Japan (BoJ) and the People’s Bank of China (PBoC) expect inflation will fall significantly in 2022 as supply bottlenecks ease and workers return to the labour market when the pandemic wanes. Thus, officials are not signaling yet that early interest rate hikes will be required to bring consumer price rises back towards their 2% targets. But the Bank of England (BoE) is likely to be the exception here and may start increasing interest rates as early as December this year as policymakers in the UK are worried that rising inflation expectations are becoming unanchored from the BoE’s 2% target. In addition, the Fed has begun tapering its quantitative easing now and some of its officials are already considering raising interest rates earlier in 2022 rather than waiting - as we expect most of the major central banks will do - until 2023 before starting to increase interest rates from their current near zero levels. Investors are thus fearful that central banks will abandon their dovish stance if inflation doesn’t start subsiding over the next few months. We will monitor these risks closely as 2022 starts. But economic activity remains far more robust as 2021 ends compared to 2020 when the virus first emerged. And we expect central banks will stay dovish if the global recovery falters - and will therefore keep supporting risk assets. The Fed remains central to 2022 prospects Central to the outlook in 2022 will be how quickly the Federal Reserve dials back the huge monetary stimulus it provided in 2020 at the start of the crisis. The Fed announced in November that it would start tapering its quantitative easing as the US economy recovers from the pandemic. The central bank will reduce its US$120 billion a month of bond buying by US$15 billion each month and end its asset purchases altogether by the summer of 2022. The Fed’s gradual exit from quantitative easing gives officials time to see if this year’s sharp increases in inflation will turn out to be only transitory. If inflation falls back to the Fed’s 2% target in 2022 as supply disruptions ease, then the central bank can keep trying to lower US unemployment by leaving its fed funds interest rate at 0.00-0.25% unchanged throughout next year. Inflation, however, is proving to be more persistent than anticipated with core measures - excluding volatile food and energy prices - increasing above 4.0% in the US now as the economy keeps reopening. Thus, the Fed may speed up its tapering and finish its quantitative easing earlier in 2022, in case policymakers decide interest rates need to be increased next year rather than waiting until 2023 to start rate hikes. Testifying to Congress on November 30, Chairman Powell hinted strongly the Fed may consider reducing its quantitative easing at a faster pace when it meets in December: “the economy is very strong and inflationary pressures are high and it is therefore appropriate in my view, to consider wrapping up the taper of our asset purchases, which we actually announced at the November meeting, perhaps a few months sooner.” Faster tapering gives the Fed the option to start rate hikes earlier from next summer if inflation remains elevated. But officials will still want to see progress on unemployment and the pandemic and will stress the bar for beginning rate hikes is higher than that for tapering quantitative easing. Thus, we retain our view that the central bank may wait until 2023 before increasing interest rates while reviewing our forecasts after each upcoming Fed meeting. We therefore see the major central banks continuing to support risk assets in 2022. We think the benchmark 10-Year Treasury yield will rise over time but only reach 1.90% over the next year, reflecting our view that overall borrowing costs will remain low despite the current surge in inflation. We note the risks are skewed towards central banks starting to increase interest rates in 2022 - earlier than we currently anticipate - if inflation doesn’t prove to be transitory. This would likely cause renewed volatility in financial markets. But our base case is for strong global growth, slow monetary tightening, and still very low government bond yields to keep benefiting risk assets as next year progresses.   Equities

Bumpy Road Ahead

Moderately risk-on in equities, with a preference for US equities. OCBC Bank, Bank of Singapore

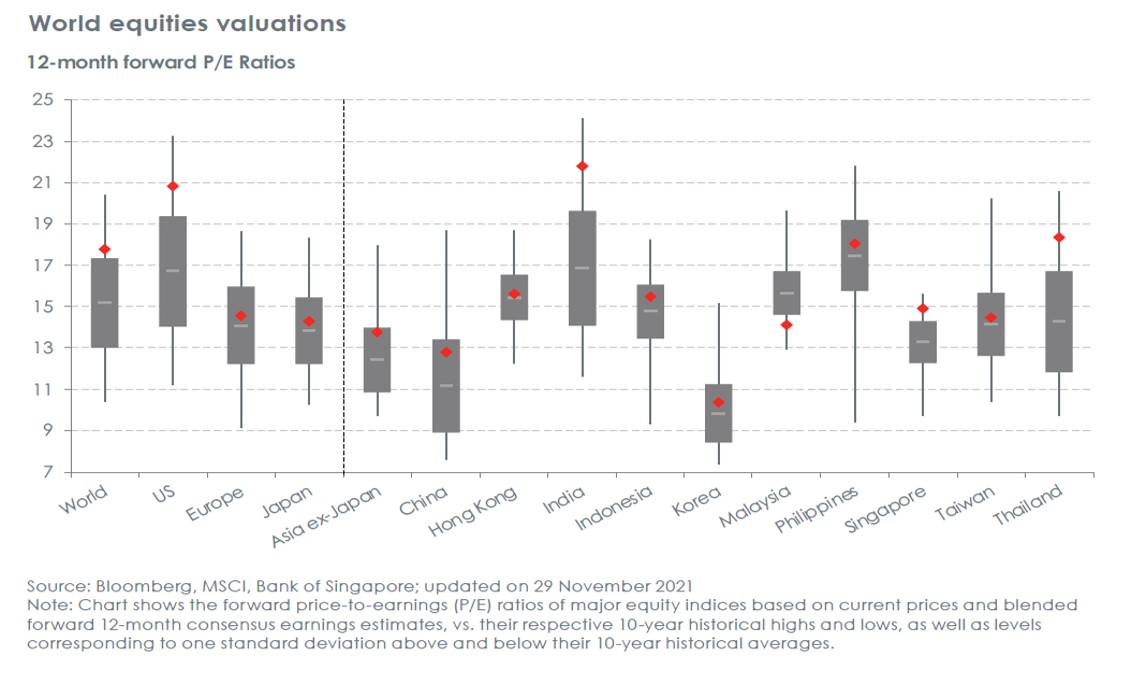

Looking into 2022, we remain constructive on equities, as expressed through our overweight position in the US. Supply chain normalisation appears to be underway, while drivers of inflation are supported by robust economic data. However, we remain mindful of tail risks, such as re-opening headwinds associated with the Omicron Covid-19 variant. We are upgrading our rating on India to ‘Neutral’ on a stabilising Covid-19 situation and buoyant economic and earnings recovery outlook for next year, partly offset by relatively high valuations. On a global sector basis, we maintain our preference for Energy, Financials, Industrials and Real Estate. The US remains our preferred spot going into 2022. In the US, inflationary pressures have been firmly in the limelight, but we believe that drivers of inflation include robust consumer demand and expansion in output driven by still-intact broad re-opening trends. We are also seeing the start of a supply chain normalisation process going into 2022, while households and corporates will likely be key sources of demand for US equities. In Europe, we note that economic recovery is coming through, though activity data in some areas do show signs of slowing on the back of factors such as supply chain constraints and high energy prices. Over the longer term, Europe’s recovery should continue, but at a moderated pace. Within Chinese equities, we re-introduce our relative preference for A-shares due to their narrowing valuation premium against the MSCI China, relatively low correlation to other markets, and greater exposure to sectors that will benefit from policy tailwinds. United States The 3Q21 earnings season was an encouraging one for the S&P500 index, with cost pressures having a more limited effect than initially anticipated. In our view, there is increasing evidence that the process of supply chain normalisation has begun, while re-opening plays could benefit as we push past the winter season. While inflationary pressures have raised concerns and led to some volatility, we believe that the drivers of inflation include robust consumer demand and expansion in output driven by still-intact broad re-opening trends that are supportive of equities. Furthermore, we think households and corporates will be key sources of demand for US equities, as they have large holdings of US cash assets as well as high cash/asset ratios, respectively. The Fed will be closely monitoring incoming data to determine how quickly to wind down its asset purchases; any adjustments to its pace of tapering could result in further market volatility. Europe Europe will continue its economic recovery eventually, but activity data is slowing in some areas in the meantime, no thanks to supply chain constraints, high energy prices and a new Covid-19 surge. On 23 November 2021, the World Health Organization warned that total deaths across Europe from Covid-19 are likely to exceed two million by March 2022. As such, a number of Western European countries have tightened mobility restrictions. That said, given that more people are vaccinated, and booster shots are also being administered, the impact on growth is likely to be milder compared to previous waves. As such, at this stage the expectation is a dent in consumption but not a derailment. Over the longer term, Europe’s recovery should continue, but at a moderated pace. We will also look out for potential Eurozone policy tensions in 2022 as policymakers face important decisions such as whether and how to rein in the very supportive monetary policy stance that was initiated in 2015 and dramatically expanded in 2020-21. Japan Japanese equities outpaced world equities in November on positive sentiment following the standalone majority won by the ruling LDP party in the lower house election and large fiscal stimulus package announced. Looking ahead, we expect more stable politics given the vote of confidence won by the Kishida administration. While the earnings season has delivered more positive surprises than negatives, the proportion of firms beating estimates moderated. We maintain a constructive stance given an improving earnings growth outlook and light foreign investor positioning. With the gradual re-opening of the economy, Japan’s GDP growth should accelerate in 2022 with further normalisation of economic activities and easing of supply disruptions. Near term, the market awaits details of the Kishida administration’s first supplementary budget, which should be supportive of domestic demand-related stocks. To re-start the economy, the government also plans to re-launch the “Go To” campaign from late January should Covid-19 remain under control. Asia ex-Japan The MSCI Asia ex-Japan Index has delivered negative returns year-to-date and underperformed other major equity indices globally. Looking ahead into 2022, we are upgrading our rating on India to ‘Neutral’, as a stabilising Covid-19 situation and buoyant economic and earnings recovery next year are offset by relatively high valuations. The MSCI India Index (MXIN Index) is currently trading at a forward price-to-earnings (P/E) ratio of 22.5x (as at 25 Nov 2021). This is near its historical peak and is two standard deviations above the 10-year average of 16.8x. Similarly, MSCI India’s forward price-to-book (P/B) ratio of 3.4x is also above its historical mean (2.6 standard deviations above 10-year mean of 2.5x). On a relative basis, MSCI India’s forward P/E ratio is at a 23.4% premium to the MSCI ACWI Index (global equity index), and this is higher than the historical average premium of 10.9% over the past 10 years. While valuations are not cheap, we believe Indian equity fundamentals appear healthy, given projected EPS growth of 34% for FY21 and 19% for FY22 for the MSCI India Index. The latter is well above the MSCI Asia ex-Japan Index average and is supported by a cyclical recovery. Given that we are also keeping our ‘Neutral’ rating on China, we see a balanced risk-reward for Asia ex-Japan as we head into 2022. China There have been tentative signs of targeted policy easing recently. The People’s Bank of China (PBOC) appeared to turn marginally more dovish and pledged to stabilise credit growth in its 3Q21 Monetary Policy report; this was not mentioned in its 2Q21 report. Going into early 2022, there could be potential front-loading of the new year’s loan and mortgage quotas – like the past few years and this would set China apart from other key developed economies that are tapering asset purchases and heading towards higher interest rates. While this would be constructive for overall market sentiment, we believe the equity market will wait for more visible and sustainable implementation. We would focus on the upcoming Central Economic Work Conference, which will discuss and set the growth targets and policies for 2022 to be endorsed at the National People’s Congress in March 2022. A more pro-growth policy tone could strengthen China’s fiscal and credit impulse early next year. We maintain our Neutral stance on MSCI China as earnings downward revisions are likely to continue (especially for offshore internet and platform industries), but we are closely monitoring the window for a potential upgrade and watching for a more pro-growth policy tone and stabilisation in earnings downward momentum. Within Chinese equities, we re-introduce our relative preference for A-shares as their relative valuation premium to MSCI China has declined. The A-shares market also has relatively low correlation to other markets and has more sectors that will benefit from policy tailwinds. We reiterate our preference for investment themes that will benefit from the 14th Five-Year Plan like renewables, new energy vehicles and their supply chain, domestic consumption and new infrastructure. Comfortable with our value/cyclical tilt Going into 2022, we remain comfortable with our value/cyclical tilt which we have moderated from an earlier heavy weighting. However, investors are advised to be more selective and adopt a stock-picking approach at current levels. Certain names in sectors exposed to positive structural trends like technology and healthcare also warrant a place in one’s portfolio, as some could be compounders over a longer time frame with their value creation prowess.  Bonds

Positive On EM High Yield Bonds

EM High Yield valuations still attractive supported by attractive valuation OCBC Bank

November turned out to be one of the most momentous months in recent memory for Fixed Income markets. Early in the month, the Fed’s long-anticipated and well-choreographed taper announcement finally came, albeit with accompanying dovish rhetoric. October’s year-over-year inflation print of 6.2% was the highest in over three decades and US Treasury bonds across the curve notched their highest yield increase since early in 2020. Additionally, Chinese Property appeared to show signs of bottoming and even recovery amidst signs that regulators and policymakers were easing up on funding and liquidity restrictions. In fixed income, we remain overweight in Emerging Market (EM) High Yield (HY) bonds, where valuations still look attractive. But we stay underweight in both Developed Market (DM) and EM investment grade (IG) bonds, as these segments face greater headwinds from rising interest rates. Better results expected for Emerging Market bonds in 2022 In EM HY, broad based regional gains were more than erased by an epic melt-down in the Chinese Property sector, leading to roughly a -2.5% return so far in 2021. In IG, a rapid rise in interest rates also contributed to a modest -0.4% return for the corresponding period, despite spread contraction. For 2022, we are expecting an improvement in HY driven by easing liquidity and better funding conditions in the Chinese property market, while in IG, the rise in rates should be more subdued than in 2021. We are forecasting a 6.75-7.0% return in HY and a 1.5-1.75% return in IG over the next twelve months. Top-down and bottom-up fundamentals broadly supportive For 2022, broad-based EM economic growth should be adequate (the IMF is forecasting 5.1% growth) and enough to underpin ongoing investment in EM corporate bonds. Company balance sheets have displayed marked improvement over the past year and robust earnings releases in recent quarters suggest ongoing credit strengthening. China HY notwithstanding, broad-based defaults remain at modest levels based on historical standards and we anticipate this trend to continue over the coming months. Valuations less challenging after a difficult year, particularly for HY Driven by concerns over excessive Chinese HY Property leverage, overall spreads in EM HY widened some ninety basis points during the year. Hence, the current valuations for HY are attractive both on a historical relative basis and versus US HY. For EM IG, spreads tightened almost twenty basis points during the year. Nonetheless, given the yield pickup over US IG, we foresee modest additional spread tightening in 2022. Overweight Asia in High Yield In HY we are raising our recommendation on Asia to overweight. Our upgrade is based on the belief that the spread tightening in Chinese Property that began in November will continue into 2022 as fine-tuning efforts from Chinese authorities to relax regulations and improve funding and liquidity continue. However, as we expect periods of volatility and additional defaults, credit selection will be critical, and we do not expect spreads to return to early 2021 levels. Chinese property sector - sentiment has turned but some more pain to come For the Chinese Property sector, there have been many signals from the regulators about easier credit to the sector. On the ground, we think banks are increasing mortgage lending faster than project loans. Overall, higher-rated players in the BBB/BB categories are still beneficiaries of the easing stance while liquidity has yet to flow to B-rated players. As a result, we think more B-rated companies will seek to extend onshore/offshore debts due in the next 1 year. While we may not revisit the confidence crisis in October 2021 before the regulators’ easing stance, the return to normalisation for the weaker players will be wrought with debt extension negotiations (or otherwise defaults), as well as efforts to raise cash via asset sales/private loans/share placements. We expect a broad-based normalisation in 2Q2022. Given the above, we prefer BBB/BB names in China HY Property sector to ride on the improvement in sentiment. They are also more resilient against uncertainties in the path to recovery. Overweight EM HY and underweight EM IG Our overweight call on EM HY is underpinned by supportive top-down and bottom-up fundamentals and attractive valuations after a difficult 2021. In IG, while rates will likely not be as big a headwind going forward, it will likely still weigh on returns. Coupled with challenging valuations, this compels us to maintain our underweight recommendation on EM IG. FX & Commodities

Cautious on Gold

Potentially higher US yield and US dollar weigh on Gold in 2022 OCBC Bank

Oil A recovery in oil price from the recent sharp decline is still possible on relief from the Omicron scare and if OPEC+ dials back its output trajectory amid the uncertainty over Omicron. We have lowered the 3-month Brent oil forecast to US$80/barrel (bbl) (old: US$85/bbl) to factor in the greater risk of countries slowing the re-opening of their borders to buy time to boost vaccination rate. Inflation, made worse by high oil prices, is becoming a political problem in the US. The US may step up ways to limit the increase in oil price beyond the recent release of strategic reserves, in coordination with other oil consuming nations. Policies to fight climate change will likely keep oil prices at higher average levels in the medium term. But the tension between policies to fight inflation versus fighting climate change could result in oil prices staying volatile. US shale producers are putting more rigs to work. High oil price will trigger higher supply that should limit price increase, which could be the story for 2022. The resumption of Iran negotiations also adds to the downside risk for oil prices in 2022. Gold Prospects for higher US real yields and a stronger US Dollar outlook are likely to weigh on gold in 2022. We target gold price to decline to US$1,620/oz by end-2022. Investors will maintain exposure to gold for diversification. But allocations are likely to be smaller than before. We expect the Fed to maintain credibility in being willing and able to head-off higher inflation. This should limit the allure of gold as an inflation hedge. Fed Chair Powell indicated that an accelerated taper of bond purchases is warranted, saying inflation is no longer transitory. If the Fed quickens the pace of tapering, the hawkish signal will likely limit further rise in inflation break-evens. However, gold prices could stay higher for longer if monetary policymakers are prompted to take a more cautious stance towards tightening. This could happen if the Omicron variant proves to be a material challenge to global recovery. Currency We have seen a resurgence of sorts for the COVID-19 pandemic, first through the rapid rise in cases in Europe and then the Omicron variant. Europe has re-imposed restrictions, to the detriment of the Euro and the European complex. The Omicron variant has not changed our macro-outlook, but it is likely to dominate market attention in early December. Our short-term playbook is a defensive one - stay short on the AUD-USD and USD-JPY as a risk hedge. Further out, we do not believe that recent COVID-19 developments will upend the monetary policy landscape into 1H 2022. The hawkish Fed continues to be the central assumption. The Fed narrative seems to be turning to a faster pace of tapering, which may then develop into possibly rate hikes in 2022. This implies the Fed may catch up with elevated market-implied rate hike expectations and this should be fundamentally US Dollar (USD) positive. In contrast, the ECB continues to cling on to the “transitory inflation” theme and prefers to keep its options open about reducing its asset purchases. This Fed-ECB divergence leaves us to be fundamentally Euro-negative. This argument extends to the Fed-BOJ space as well. We prefer to be long the USD-JPY beyond the immediate risk-off episode. The RBA have scope to be more neutral, especially if the elevated commodity complex supports the external sector. We thus reduce our AUD-negative bias for the medium term. In Singapore, the heavy Singapore Dollar (SGD) nominal effective exchange rate (NEER) appears to run contrary to the domestic macro-outlook. The base case scenario remains for another slope steepening move in the April 2022 MAS Monetary Policy Statement. Thus, the SGD NEER should stay supported into 1Q 2022. For now, dips should be seen as an opportunity to enter long SGD basket trades with a medium-term time horizon. |

||||||||||||||||||

|